The concept of the “stock market” often conjures images of frantic men in suits shouting on a trading floor, or perhaps complex charts flashing across multiple screens in a high-tech office. For many, it feels like an exclusive club reserved for the wealthy or the financial elite. This perception, however, is one of the biggest barriers to financial freedom.

The truth is that the stock market is simply a marketplace—a tool that allows ordinary people to participate in the growth of the global economy. It is not a casino, provided you approach it with a strategy rather than a gamble. Investing is one of the most reliable ways to build wealth over time, outpace inflation, and secure a comfortable future.

If you are standing on the sidelines waiting for the “perfect time” to start, the answer is: today. This comprehensive guide will walk you through everything you need to know to go from a complete novice to a confident investor.

Part 1: The “Why” – Understanding the Necessity

Before discussing how to invest, it is crucial to understand why you need to do it at all. Why not just keep your money in a savings account?

The answer is Inflation. Inflation is the silent erosion of your purchasing power. If a loaf of bread costs $2.00 today, it might cost $2.10 next year. If your money is sitting in a standard bank account earning 0.01% interest, your money is technically “safe,” but its value is shrinking. You can buy less with that money next year than you can today.

Investing is the act of making your money work for you so that it grows faster than inflation eats it away. The stock market, historically, has provided an average annual return of roughly 10% (before inflation) over the last century. By investing, you are not just saving money; you are preserving and growing your life’s energy.

Part 2: The Pre-Flight Checklist

Investing involves risk. The market goes up, but it also goes down. Because of this volatility, you need a solid financial foundation before you expose your hard-earned money to the market. Do not skip these three prerequisites:

1. The High-Interest Debt Trap

Imagine trying to fill a bucket with water while there is a massive hole in the bottom. That is what investing is like when you have high-interest consumer debt (like credit cards).

- The Math: If the stock market returns an average of 10% per year, but your credit card charges you 20% interest, you are mathematically losing 10% by investing.

- ** The Move:** Pay off all high-interest debt first. Paying off a 20% debt is the equivalent of getting a guaranteed, risk-free 20% return on your money.

2. The Emergency Fund

Life is unpredictable. Cars break down, medical emergencies happen, and layoffs occur. If you have all your money tied up in stocks and you suddenly need cash, you might be forced to sell your investments at a loss.

- The Goal: Aim to have 3 to 6 months of living expenses in a separate, easily accessible High-Yield Savings Account (HYSA). This is your insurance policy that allows your investments to grow uninterrupted.

3. Define Your Time Horizon

Money you need in the next 1–3 years (for a wedding, a house down payment, or a vacation) belongs in a savings account or a Certificate of Deposit (CD), not the stock market. The market is volatile in the short term. Investing is for money you can leave untouched for at least 5 to 10 years.

Part 3: What Are You Actually Buying?

When you open a brokerage account, you will face a menu of options. Here is a breakdown of the primary assets you need to understand.

A. Individual Stocks (Equities)

When you buy a “share” of a company—say, Microsoft or Coca-Cola—you become a partial owner of that business. You are a shareholder.

- How you make money:

- Capital Appreciation: The stock price goes up because the company becomes more valuable.

- Dividends: The company distributes a portion of its profits directly to shareholders as cash payments.

- The Risk: High. If that specific company makes a bad product, faces a lawsuit, or goes bankrupt, your investment tanks.

B. Bonds

When you buy a bond, you are essentially lending money to a government or a corporation. In return, they pay you interest (a “coupon”) and eventually pay back the loan amount.

- The Risk: Generally lower than stocks. Bonds are often used to stabilize a portfolio.

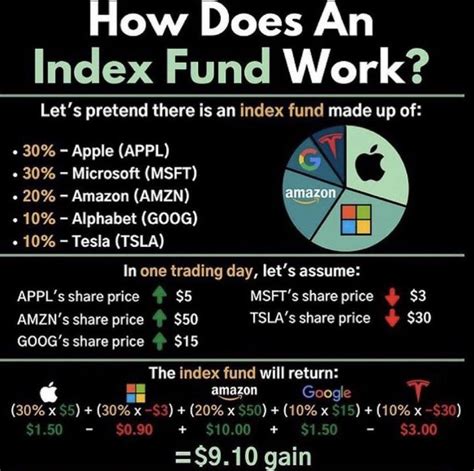

C. Exchange Traded Funds (ETFs) and Index Funds

This is the “sweet spot” for beginners. Instead of trying to pick the one “winning” stock (which is incredibly difficult, even for professionals), you buy a basket of stocks.

- How it works: An Index Fund tracks a specific market segment. For example, an S&P 500 Fund buys small pieces of the 500 largest companies in the US.

- The Benefit: Instant diversification. If one company in the basket fails, you have 499 others to prop you up. You get the average return of the market, which historically beats most professional stock pickers.

Part 4: Developing Your Strategy

Now that you know what to buy, you need a strategy for how to buy it. The best strategy for beginners is boring, repetitive, and highly effective.

The Power of Dollar-Cost Averaging (DCA)

New investors often obsess over “timing the market.” They try to buy at the lowest possible price and sell at the highest. This is a fool’s errand; nobody knows what the market will do tomorrow.

Instead, use Dollar-Cost Averaging. This involves investing a fixed amount of money at regular intervals, regardless of the share price.

- Example: You invest $200 on the 15th of every month.

- Month 1: Prices are high. Your $200 buys 2 shares.

- Month 2: Prices crash. Your $200 buys 4 shares.

- Month 3: Prices stabilize. Your $200 buys 3 shares.

- The Result: You automatically buy more shares when they are “on sale” and fewer when they are expensive. This lowers your average cost per share over time and removes the emotional stress of watching stock tickers.

The Magic of Compound Interest

Albert Einstein reportedly called compound interest the “eighth wonder of the world.” Compounding is what happens when your earnings generate their own earnings.

- Year 1: You invest $1,000 and make 10% ($100). You now have $1,100.

- Year 2: You make 10% again. But now, you make 10% on $1,100, which is $110.

- Year 30: That original money has multiplied exponentially, not linearly.Time is your greatest asset. Starting at age 25 gives you a massive advantage over starting at age 35, simply because your money has ten extra years to compound.

Part 5: How to Execute (Step-by-Step)

Step 1: Choose a Brokerage Account

You need a platform to buy and sell.

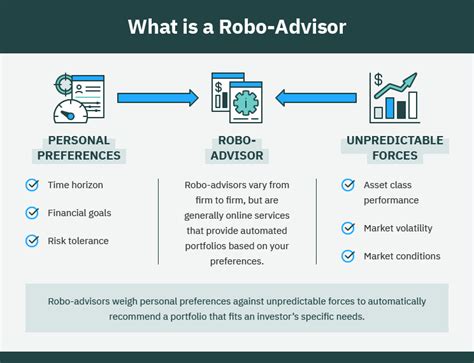

- Robo-Advisors (e.g., Betterment, Wealthfront): These are “set it and forget it.” You answer a quiz about your risk tolerance, and an algorithm builds and manages a portfolio for you for a small fee.

- Discount Brokers (e.g., Fidelity, Vanguard, Schwab): These allow you to buy stocks and ETFs yourself. Look for platforms with zero trading commissions and no account minimums.

Step 2: Open the Account

This is usually as simple as opening a bank account. You will need to provide identification and link a funding source (your checking account).

Step 3: Select Your Investment (The “Three-Fund Portfolio”)

You don’t need to complicate things. A popular strategy is the “Three-Fund Portfolio,” which covers the entire world:

- Total US Stock Market Index Fund: Covers all US companies.

- Total International Stock Market Index Fund: Covers companies outside the US.

- Total Bond Market Fund: Provides stability (add more bonds as you get older/closer to retirement).

Note: Many beginners start with just an S&P 500 ETF or a “Total World” ETF for simplicity.

Step 4: Automate It

Go into your brokerage settings and set up an automatic transfer and purchase. For example: “Transfer $100 every payday and buy [Chosen ETF].” This removes the temptation to spend the money elsewhere.

Part 6: The Psychological Barrier

The hardest part of investing is not the math; it is the psychology.

Managing Volatility

The stock market is volatile. In 2008 and 2020, the market dropped significantly. When this happens, human nature screams, “Sell everything before I lose it all!” This is the wrong move. You only lose money if you sell. If you hold through the crash, you still own the same number of shares, and historically, the market eventually recovers and reaches new highs.

- Mantra: “Time in the market beats timing the market.”

Avoiding FOMO (Fear Of Missing Out)

You will hear stories of people getting rich overnight on “meme stocks” or the latest trendy cryptocurrency. It is tempting to chase these trends. Resist. Boring investing is profitable investing. Trying to chase the “next big thing” usually results in buying at the top and losing money when the hype dies down. Stick to your index funds and your long-term plan.

Conclusion: The Best Day to Plant a Tree

There is a Chinese proverb that says: “The best time to plant a tree was 20 years ago. The second best time is today.”

Investing works the same way. You may wish you had bought Amazon stock in 1997, but dwelling on the past won’t build your future wealth. The barrier to entry has never been lower. You can start with $50, $20, or even $5 thanks to fractional shares.

The path to financial independence is not a sprint; it is a marathon. It requires patience, discipline, and the courage to start. By following the steps in this guide—building your safety net, choosing diversified funds, automating your contributions, and ignoring the noise—you are taking control of your financial destiny.